Recent case study

Credit Market Update

Leveraged loans & high-yield bonds

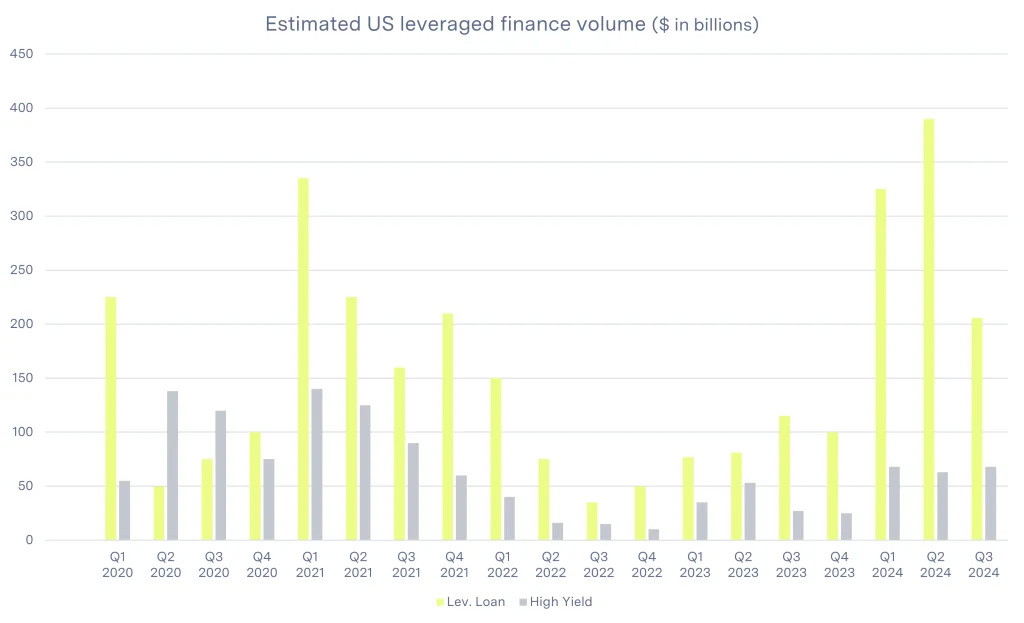

Leveraged loan issuance has had a record year as high-yield bonds have posted a strong recovery (compared to 2022 and 2023), driven by robust investor demand and improving spreads, creating supportive conditions for issuance across borrowers of all credit quality. U.S. leveraged loan volumes in 2024 (through Q3) soared ~300% compared to the same nine-month period in 2023 ($922 billion across 842 transactions), while high-yield bond issuance saw a ~50% uptick year-over-year through Q3 2024 ($199 billion across 263 transactions).

Lenders are willing to deploy capital and can achieve attractive yields lending into the more distressed situations, and borrowers are happy to access this readily available capital to refinance with looser protections (“covenant-lite” structures), facilitating the “kick-the-can” strategy. To this point, the strong issuance in 2024 has driven significant progress on the ~$2.1 trillion 2025/2026 maturity wall, as approximately $892 billion (~79%) of the leveraged loan and high-yield bonds issued through the end of Q3 2024 were refinancings and recapitalizations, while only ~16% were acquisition-related (with the remainder for general corporate purposes).

Source: Source: Debtwire (estimate).

Despite the high issuance across the credit risk spectrum, credit markets continue to see near COVID-era default rates and credit downgrades, partially attributable to the current elevated interest rate environment and sustained operational headwinds driven by inflation and supply chain disruption.

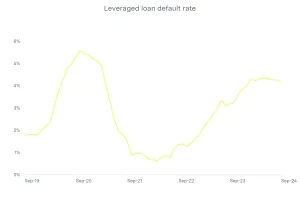

The leveraged loan LTM default rate (including distressed exchanges) ended Q3 2024 at 4.2%, modestly lower than the prior quarter (4.3%), though well above the ~1.0% levels seen in 2022. Distressed leveraged loan transactions on an LTM basis are most concentrated in the healthcare equipment & services sector (27% of activity) and the software & services sector (23% of activity). In the third quarter of 2024, loan downgrades outpaced upgrades by 2.1x, consistent with the prior quarter.

Source: PitchBook | LCD. Leveraged loan default rate on an LTM basis and includes distressed exchanges.

The rise in defaults and heightened downgrades should be monitored closely as these are typically leading indicators of forthcoming restructuring activity. In fact, default rates and downgrades as a proxy for distress may be somewhat understated given the increased LME activity currently being undertaken.

Private credit

To address credit opportunities outside of “down the fairway” direct lending (which mimics traditional bank lending, but with the benefits of flexibility and speed at a higher cost of capital), credit managers have developed more aggressive and sophisticated lending solutions to build market share and put capital to work. As a marker, nearly 30% of private debt fundraising through Q3 2024 was via special situations or mezzanine/junior debt, with Oaktree (~$18B) and Blackstone (~$10B) opportunistic funds accounting for two of the top ten largest private debt fundraises in 2024.

Further, weakening fundamentals for private credit portfolio companies have driven negative ratings actions in 2024, as the number of issuers rated B (negative outlook) or lower represented over 30% of rated middle-market issuers (compared to 20% in 2023). As a result, the pace of downgrades and default events has materially increased for private credit borrowers.

Distress is also visible via rising non-accrual rates in BDC portfolios, which are now near 2020 levels. On average, across seven large-cap BDCs, non-accruals represented 2.4% of the portfolio at cost, compared with the COVID-era peak of ~3.0%—significantly higher than post-COVID lows (1.1%). Given that private capital providers enjoy more flexibility in loan structuring and greater risk tolerance compared to the traditional loan market, an increase in BDC non-accrual rate is likely to lead to an increase in LMEs.

Source: Quarterly Filings of BDCs used within data set.

Liability management exercises

Borrowers are increasingly viewing LMEs as pragmatic and effective structural mechanisms to “buy time” and improve recovery positions in the face of looming debt maturities and liquidity cliffs. The objectives of utilizing LME structures are generally to enhance the borrowers’ liquidity, provide near-term financial relief related to maturities, enhance profitability, and allow stakeholders a longer runway to make better decisions during challenging business cycles. Additionally, the rising cost of in-court restructurings has driven some borrowers to seek out-of-court alternatives, including:

- Cash tenders/buybacks

- Credit agreement “amend-and-extend” transactions

- Distressed debt for equity exchanges

- Drop-downs/double-dips (unrestructured subsidiary financings)

- Consent solicitations

- Up-tiering debt recapitalizations

The proliferation of LMEs in 2024 has forced both creditors and debtors to rethink how they organize and approach negotiations. Creditors have developed strategies to position themselves for LME transactions ahead of management-developed proposals, including entering into cooperation agreements (“co-ops”) among creditors to put forth LME solutions to address near-term liquidity and credit-related concerns. Co-ops have soared in 2024, with 45 agreements completed YTD compared to four in total between 2018 and 2023.

While co-ops are intended to reduce risk and increase the ease of execution across parties, the ultimate legality of such structures may be tested due to the complexity and nuance baked into these agreements. Priming creditors can benefit from attaining seniority in the capital structure, while existing creditors may in turn receive a significant discount to fair market value. As a result, the legitimacy of these transactions could be questioned in litigation, as was the case for the exchange offer in the proposed merger between DISH Network and EchoStar Corporation in late 2023/early 2024.

While LMEs often signal a less than 100% recovery rate for existing lenders, the immediate pro forma liquidity profile is significantly improved, therefore allowing the borrower to continue operations free of creditor distraction and to chart a path to profitability as priming lenders increase their seniority in the capital stack. Below is a snapshot of Q3 2024 LMEs and the subsequent credit ratings movement.

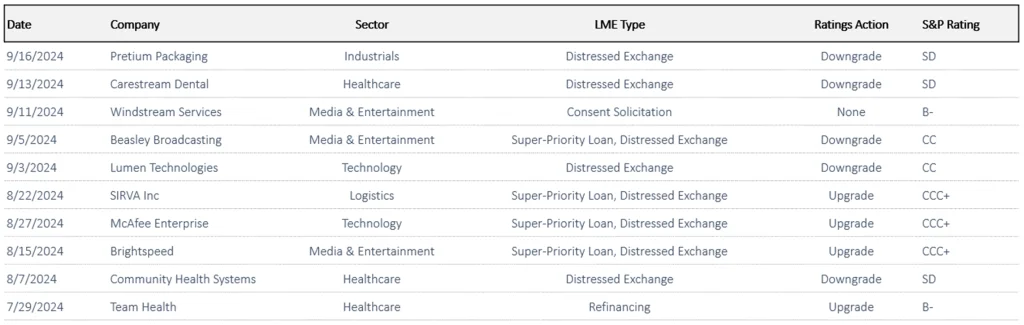

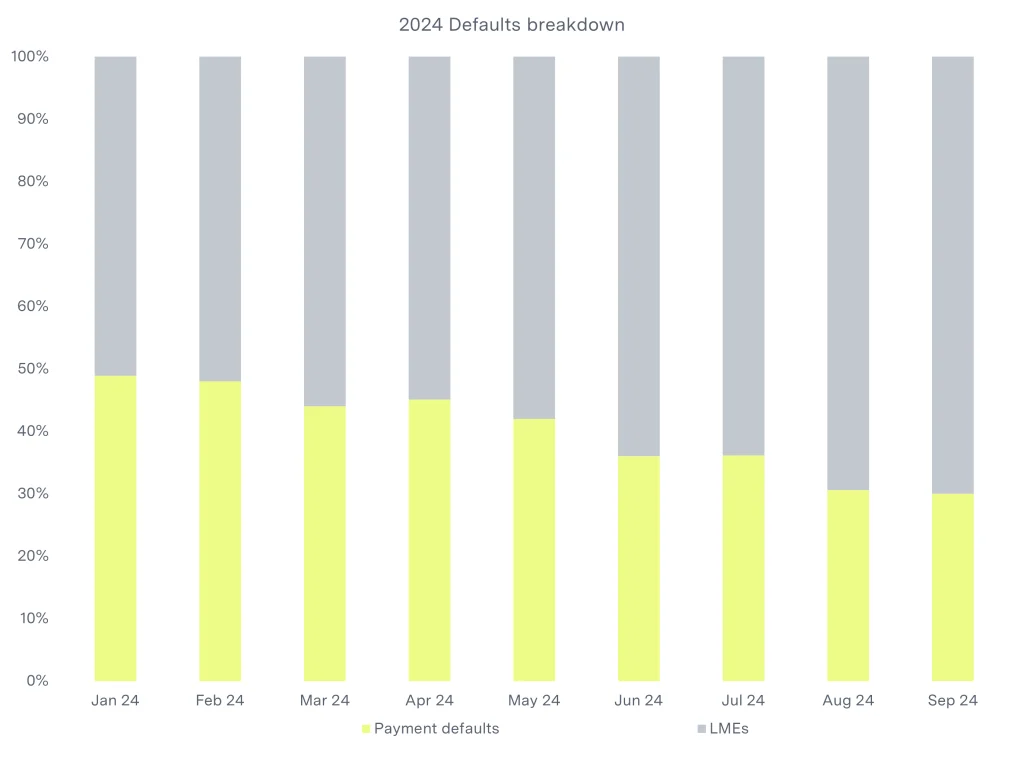

Distressed exchanges have paved the way for a shift in the default landscape in Q3 and Q4 2024. Rather than pursuing in-court restructuring options, companies are opting for “soft defaults” via LMEs at a higher clip (~68% of Q3 2024 restructurings) to reposition their balance sheets. By comparison, roughly half of U.S. defaults resulted in some type of distressed exchange or LME in 2023, and only ~20% – 30% in the mid-2010s.

Source: PitchBook | LCD.

Overall, LMEs have been strategically deployed at a more frequent rate than traditional restructurings as the need for a liquidity buffer and looming maturities have pushed borrowers to act quickly. While lenders are increasingly hungry to deploy capital in creative ways to at-risk borrowers, the incremental liquidity often isn’t sufficient to prevent the debtor from subsequently undergoing a more costly in-court restructuring.

Conclusion

Distress trends largely represent a continuation from the prior quarter, with leveraged loan default rates and BDC non-accrual rates remaining near COVID-era peaks. Credit market conditions suggest more defaults may be looming due to prolonged cost pressures and high financing costs that have continued into Q4 2024. We anticipate continued momentum in restructuring activity as out-of-court processes, including LME transactions, will remain a preferred initial strategic choice. Despite the perceived near-term benefits of such structured solutions, borrowers and lenders may need to consider a more traditional process to successfully restructure troubled credits—and the underlying businesses—for the long-term.

Additional sources

- PitchBook | LCD

- PitchBook

- S&P Capital IQ Pro

- Debtwire

- Industry Research

- Fitch Ratings

- International Monetary Fund

- Company earnings call transcripts and presentations

- BDC data set:

- Ares Capital Corporation

- Blackstone Secured Lending Fund

- FS KKR Capital Corporation

- Golub Capital BDC, Inc.

- Goldman Sachs Business Development

- Blue Owl Capital Corporation

- Sixth Street Specialty Lending