BOTTOM LINE UPFRONT

New England CFOs are outperforming their peers on exit readiness — and it still isn’t enough. Sponsors are underwriting against absolute readiness, not relative progress. The gaps in timing, audit continuity, scenario planning, and AI adoption are showing up in valuations now, well before any sale process begins.

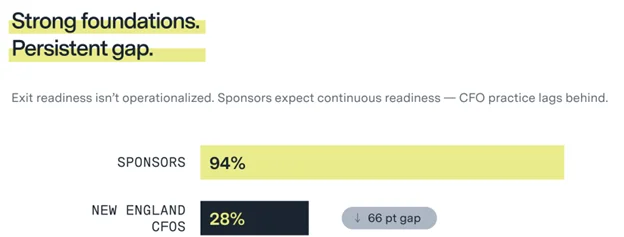

There’s good and bad news for New England-based CFOs: they’re closer to exit ready than their national peers, but they’re still behind where sponsors want them. In fact, Accordion’s survey of New England-based sponsors and CFOs shows that expectations are far outpacing execution.

And as exit windows reopen, readiness gaps are surfacing earlier: in audits, in lender conversations, and in sponsor reviews. Which means exit readiness is no longer a phase triggered by a sale process. It’s an operating condition that directly influences valuation, timing, and negotiating leverage – and for NE CFOs, “closer than peers” is no longer enough.

The bar has moved

After years of constrained exit activity, private equity is moving from patience to pressure. Median holding periods are approaching seven years, DPI remains uneven, and sponsors are managing aging assets amid growing LP pressure to return capital.

And as hold periods grow, so too do sponsor expectations. Sixty-four percent of sponsors say extended hold periods materially raise expectations for CFO performance, yet only 45% of NE CFOs report adjusting their approach during longer holds

In this environment, sponsors are no longer waiting for a fully reopened deal market to demand readiness… and they can’t. Rates remain elevated, tariff uncertainty clouds forward visibility, and there’s no clear signal on when conditions will stabilize.

So they’re preparing for speed. Exit windows may open opportunistically and close quickly. The companies that require six months of internal clean-up, accounting remediation, or KPI redefinition won’t be able to capitalize. Those that used extended hold periods to get exit ready will.

Where expectations are outpacing execution

Our survey data points out exactly where the gaps in sponsor expectations vs. reality lie:

1. The timing gap

Eighty-seven percent of sponsors expect exit preparation to begin 18-24 months before a sale, yet only 35% of NE CFOs start that early – with nearly half still relying on a three-to-six-month preparation sprint and some even beginning prep with less than three months before launch.

In other words: two-thirds of CFOs aren’t getting exit ready early enough. When preparation is compressed, CFOs are forced into documentation mode rather than optimization mode. Initiatives remain partially implemented. Reporting processes remain newly established. Narrative refinements remain untested. Buyers tend to discount unfinished work and partially embedded improvements, often pricing in risk rather than potential.

Sponsors increasingly interpret compressed preparation windows as a signal that value creation has not been fully institutionalized. Discounted valuations are the result.

2. The audit readiness gap

NE-based CFOs seem to be in good shape when it comes to audit readiness; 71% prioritize audit-ready financials, 13 points higher than their national peers. So why do one-third of these CFOs still enter audit cycles unprepared?

Because audit readiness is no longer a year-end milestone (though many CFOs still treat it as such). It’s a continuous signal of exit preparedness. Where audits slip, delays cascade: fees increase, lender deadlines tighten, and management inevitably shifts from strategy execution to reactive issue resolutions.

And even immaterial findings can expand diligence scope. Buyers won’t just react to the issues, but they’ll also question the reliability of the underlying financial infrastructure. That uncertainty is often priced in.

3. The scenario planning gap

NE-based CFOs are ahead of the game when it comes to technical discipline. But clean financials don’t necessarily mean continuous and buyer-defensible readiness: 52% of sponsors cite scenario planning as a weakness, and 43% point to inconsistent KPI tracking.

Even strong financial performance (and technical accounting readiness) can fall short if it isn’t supported by credible scenario modeling and consistent, visible metrics: assumptions insufficiently pressure-tested, KPIs lacking continuity, and performance untethered to value creation outcomes.

Buyers are assessing whether the numbers can stand up to scrutiny. What isn’t clearly demonstrated isn’t fully valued.

4. The AI gap

Eighty-five percent of buyers now factor AI-enabled finance into valuation discussions, yet only 34% of NE CFOs have embedded it into workflows.

With AI as the conversation right now, most finance teams are at least exploring AI. But few have actually operationalized it in forecasting, analytics, or decision-making. Which means that in most portfolio companies, AI is not yet signaling the data maturity, scalability, and management sophistication that buyers expect it to.

In an environment where buyers are underwriting where a business is going – and how well it can scale under new ownership – limited adoption is increasingly viewed as a sign of hesitation.

The bottom line? Make exit readiness a permanent state of mind

Exit readiness has evolved from a transaction milestone to a permanent operating posture. And while NE CFOs are closer than their national peers in some important areas, sponsors today are underwriting against absolute readiness. Not relative improvement.

The bar is higher, and so are the stakes. Until continuity, buyer-visible signaling, and forward-looking conviction match foundational strength, the gap will remain priced into outcomes.